An article that just appeared in the journal Global and Planetary Change, authored by me and Mark Freeman and Michael Mann, reported a simulation experiment that sought to put constraints on the social discount rate for climate economics. The article is entitled Harnessing the uncertainty monster: Putting quantitative constraints on the intergenerational social discount rate, and it does just that: In a nutshell, it shows how a single, policy-relevant certainty-equivalent declining social discount rate can be computed from consideration of a large number of sources of uncertainty and ambiguity.

In the previous two posts, I first outlined the basics of the discounting problem and highlighted the importance of the discount rate in climate economics. In the second post, I discussed the ethical considerations and value judgments that are relevant to determining the discount rate within a prescriptive Ramsay framework.

I showed that those ethical considerations can yield unresolvable ambiguity: different people have different values, and sometimes those values cannot be reconciled. Fortunately, in the discounting context, we can “integrate out” those ambiguities by a process known as gamma discounting. This is the topic of the remainder of this post.

A final post explains our simulation experiment and the results.

Gamma Discounting

We know from the last post that in a recent survey of 200 experts, Moritz Drupp and colleagues found that the distribution of expert responses was closely approximated by setting δ to zero with 65% probability and setting it to 3.15 with 35% probability. (If you don’t know what d refers to, please read the previous post first.)

It turns out that recent work in economics has proposed a way to resolve such ambiguity or uncertainty. This process is known as gamma discounting. In a nutshell, instead of averaging the candidate discount rates, the process averages the discounted future values for each candidate rate.

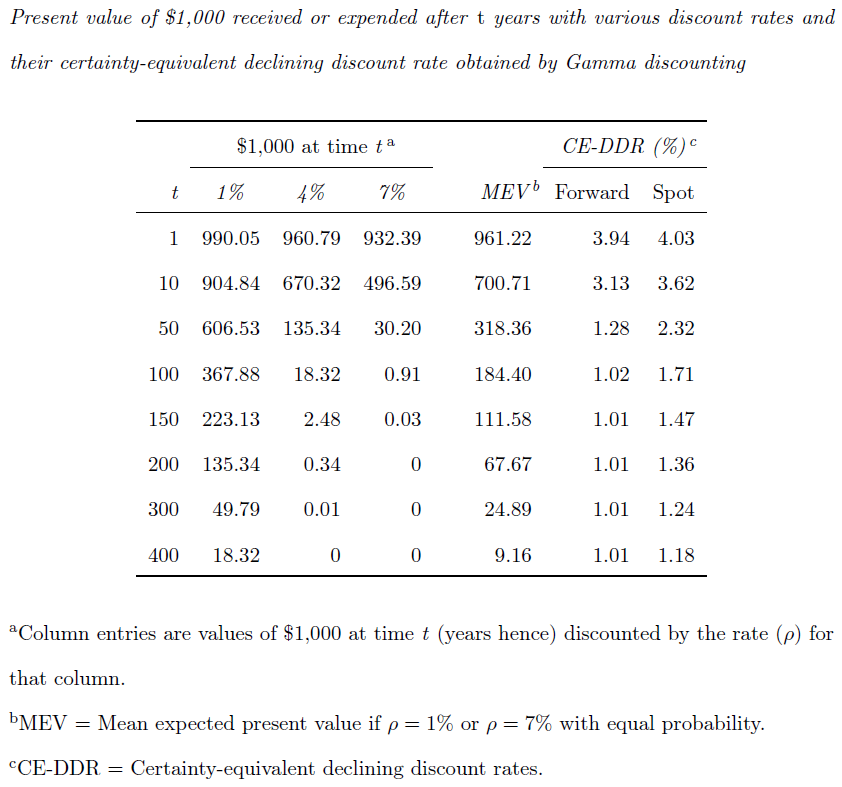

The table below illustrates gamma discounting using an example provided by Ken Arrow and colleagues.

The table shows discounted values of $1,000 at various times t in the future for three different candidate discount rates (namely, 1%, 4%, and 7%). For example, if the rate is 4%, then the discounted value of $1,000 after 50 years is $135.34, and so on.

So how do we deal with the uncertainty about the discount rate? Suppose we assume that the rate is either 1% or 7% with equal probability, then 50 years from now our $1,000 can be worth either $606.53 or $30.20 (also with equal probability).

It follows that the average of those two uncertain values represents the probability-weighted expectation for our $1,000, which 50 years from now is ($30.20 + $606.53)/2 = $318.36.

These averages are called the “mean expected present values” and are shown in the column labeled MEV. They form the basis of our final computation. The ratio between successive MEVs yields a single certainty-equivalent discount rate (columns labeled CE-DDR) for any given point in time. For example, the MEV at t = 50 is $318.36, and the MEV at t = 51 is $314.33. The ratio between those successive values, $318.37/$314.33 = 1.0128 = 1.28%, provides the CE-DDR at time t = 50, known as the “forward” rate, and those values are shown in the second-to-last column of the table.

Several important points can be made about that column: First, there is only one column. No matter how many candidate discount rates we started out with, and what their probability weighting might be, we end up with a single certainty-equivalent discount rate that can be applied with 100% certainty, but that has embedded within it the uncertainty we started out with.

Second, the discount rate is not constant: as can be seen in the table, it starts out at nearly 4% and converges towards 1% after 100 years or more. The discount rate is therefore declining over time. (In the limit, when time heads towards infinity, the discount rate converges towards the smallest candidate rate being considered. The choice of lowest candidate rate is therefore crucial, although this primarily affects the distant future.)

Finally, the second-to-last column captures the slope of the declining discount rate function between times t and t + 1. Those forward values, however, cannot be used to discount an amount from the present to time t—for example, the MEV at time t = 50 cannot be obtained by discounting $1,000 at a rate of 1.28% over 50 years.

Instead, to obtain a rate that covers all of those 50 years, we need a different certainty-equivalent discount rate that is also declining but generally has higher values. This rate is called the “spot” certainty-equivalent declining discount rate and is shown in the final column.

If we apply the “spot” rate to our present-day $1,000 for time t, it will yield the MEVs for that time shown in the table. For example, $1,000 discounted at 2.32% over 50 years (i.e., 1000/1.023250) yields the MEV of $318 (± rounding error).

To summarize: We start out by being uncertain about the discount rate. For example, we don’t know whether to set the pure time preference to zero or to permit a value greater than that. We apply gamma discounting and this uncertainty has “disappeared”. Of course, it hasn’t really disappeared, it has just been taken into account in the final certainty-equivalent discount rate.

But for all practical intents and purposes, we now have a single number that we can apply in economic decision making.

In the first post, we considered the implications of the discount rate if climate change were to cause $5 trillion (i.e., $5,000,000,000,000) in damages by the end of the century. We noted that the present discounted cost could be as large as $2.2 trillion (discount at 1%) or as little as $18 billon (at 7%). If we assume that 1% or 7% are equally likely to be “correct”, then from the table above we can obtain a certainty-equivalent spot rate of somewhere below 2% (the end of the century is 83 years away, but that’s reasonably close to the 100 years that yield a spot rate of 1.71%).

It follows that to avert $5 trillion in damages, it would be economically advisable to expend in excess of $1 trillion now on climate mitigation even if we are uncertain about which discount rate to apply.

Combining sources of uncertainty

This post explained the basic idea behind gamma discounting. We now have a mathematical platform to convert ambiguity and uncertainty about the discount rate into a single certainty-equivalent discount rate.

The beauty of gamma discounting is that it is theoretically particularly firmly grounded when the candidate discount rates (the first three columns in the above table) arise from irreducible heterogeneity among expert opinions rather than from random variation about an imprecise estimate.

Different ethical positions about inequality aversion (η; see previous post) and pure time preference (δ) are clear instances of such irreducible heterogeneity. In our simulation experiment, we considered the uncertainty about three other relevant variables as similar cases of irreducible heterogeneity; namely, uncertainty about climate sensitivity, uncertainty about emissions policy, and uncertainty about future global development.

To briefly foreshadow the final post, we conducted a simulation experiment that forecast economic growth till the end of the century under all possible combinations of those variables. We then applied gamma discounting as in the table above to extract a single certainty-equivalent declining discount rate that policy makers can apply in the knowledge that a broad range of uncertainties has been considered.

The bars on the left show belief ratings for facts after they were affirmed across three retention intervals. It can be seen that affirmation raises belief above the pre-intervention baseline (the dotted line), and that the increase in belief ratings is remarkably stable over time (we can ignore the ‘brief’ vs. ‘detailed’ manipulation as it clearly had little effect).

The bars on the left show belief ratings for facts after they were affirmed across three retention intervals. It can be seen that affirmation raises belief above the pre-intervention baseline (the dotted line), and that the increase in belief ratings is remarkably stable over time (we can ignore the ‘brief’ vs. ‘detailed’ manipulation as it clearly had little effect).